If you're learning about debt review, you might hear the term “PDA”. In the debt review context, PDA stands for a Payment Distribution Agent. These are companies registered with the National Credit Regulator (NCR) to handle payments for consumers in debt review.

What Do PDAs Do?

PDAs make debt review payments simple.

Instead of paying multiple creditors individually, a consumer makes one monthly payment to the PDA, which then distributes the funds according to the debt review plan. This ensures payments are made on time and in the correct amounts, reducing errors and stress.

Do PDAs Charge Fees?

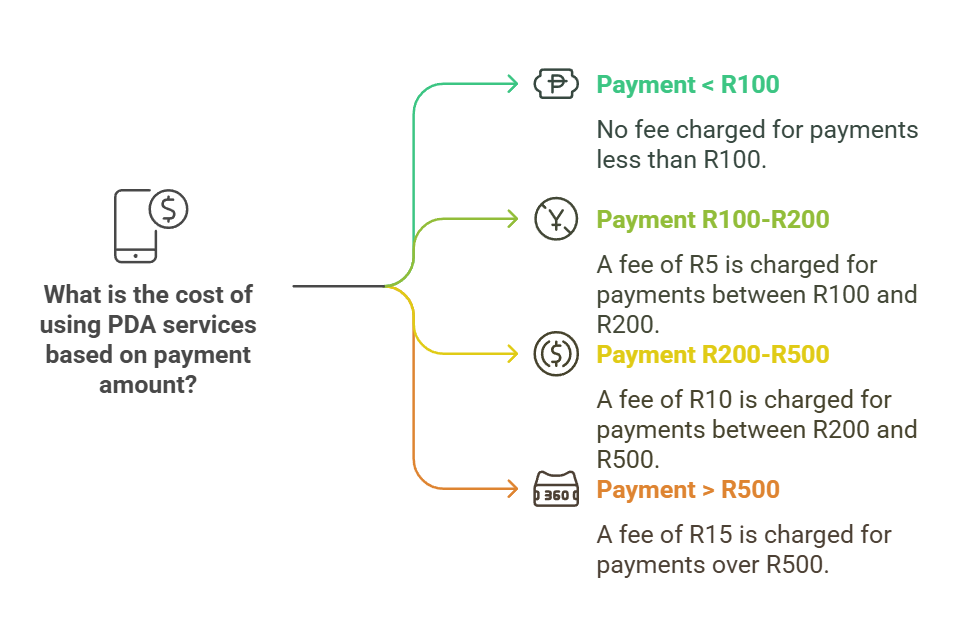

Yes, PDAs charge small fees based on the payment amount:

These fees cover tracking and distributing funds accurately as well are sending you statements monthly.

Are PDAs Safe?

Yes. Using a PDA is very safe and convenient.

The NCR monitors and audits PDAs all the time, ensuring consumer funds are handled securely. PDAs also have external auditors that make sure your funds are safe.

Beware of Scams

PDAs never change their bank details!

If someone asks you to pay into a different account, contact your Debt Counsellor and PDA immediately. Beware!

NCR Recognized PDAs in South Africa?

Currently, the National Credit Regular approved PDAs are:

- DC Partner PDA

- Hyphen PDA

- iPDA

If you’re feeling overwhelmed by debt, you don’t have to face it alone. Contact us today or apply now to begin your debt review journey. Our caring, experienced team of Debt Counsellors will walk with you every step of the way — from your initial assessment right through to receiving your Clearance Certificate. Don’t let debt steal another day of peace. Take the first step toward lasting financial freedom with Debt Solutions today.